Supermarkets – at least in Switzerland – temporarily cut prices for a bunch of products every week. There are many good reasons for discounting products. Long run effects on quantity sold by accelerating the diffusion of new products or simply getting new customers with a lower willingness to pay to try the product. Comestible goods may be close to their expiration date and are better sold at a lower price than disposed at a cost. Storage place may be needed. Discounting may also be a reaction to the price behaviour of competitors or part of a strategy to build or maintain a low price image.

All these reasons for temporary price actions may make sense. Another reason for temporary discounts might be, to achieve a higher surplus by selling higher quantities at a lower price. In the following, I argue that this last reason for discounting is probably not a good one in many cases.

First, we have to consider that a price reduction erodes the profit margin disproportionately because of the variable product-costs. So, if the discount on the selling price is 20 %, then the decrease of the profit margin may be e.g. 50 %. That means, we must sell double quantity to achieve the same total profit during the discounting as with the prevailing price.

Hence, to cover the effect of a lower margin, we already need a respectable increase in the sold quantity. But this is only part of the story. Different kind of substitution effects increase the quantity needed, only to achieve the same surplus as with the normal price. In the following, we discuss an example with a temporary price discount on a mineral water “A”, which reduces the profit margin to 50 % of the margin with usual price. The conclusions can easily be generalized.

The first effect to address is substitution along time. Is it enough to make the discount action an economical success, when the average customer buys more than double quantity, than he would at usual price? This is not the case, when he substitutes the purchase of mineral water “A” in our store in the future. If the substitution is perfect, the discount action is a loss, because customers buy beneficially today, what they would have bought in the future at a higher price. Only the quantity the don’t buy at our competitors ad to the double quantity we need to cover the lost margin, while the sales we loose in the future have to be deducted twofold.

If price discounts are announced, what is very common in Switzerland, then the substitution along time starts even before the discounting has started. Customers anticipate it and wait until they can buy cheaper.

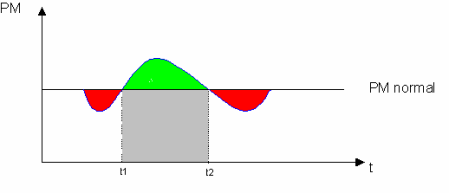

The following figure shows our results so far:

The ordinate shows profit contribution and the abscissa represents time. The black line displays the (normalized) daily profit at the usual product price, while the blue curve describes the (exemplary assumed) progression of daily profit during a discount campaign. The two red areas represent the lost profit trough substitution along time, which takes place before and after the discount campaign, starting in t1 and ending in t2.

The green area displays the excess profit that possibly can be achieved during the discount campaign. But remember: To get in the green area of excess profit, we have to sell more than double quantity of the discount mineral water (indicated by the grey shaded area)! Moreover, the green area has to cover the losses before and after the campaign (thus, the two red areas), where one lost unit has to be compensated twice during the campaign.

So far we notice, that a huge excess quantity is needed, to simply reach the same profit margin as usual, when we drive a discounting campaign. But still we are far from the bottom line. The next topic to address is substitution among products.

In a supermarket, many products are substitutes for one another. To some extent, every food product or every beverage can be replaced by another in the same store. The same appears for toothpaste, shampoos, batteries etc. Supermarkets usually offer a variety of these products, and customers may switch, when there are price changes.

If we return to our mineral water campaign, we can presume, that some customers originally wanted to buy another mineral water, fruit juice or soft drink, when they entered the store. But then they switched to mineral water “A”, because they saw, that it is at a discount. Hence, some of the additional sold quantity of mineral water “A” comes along with a lost sale of another beverage. We can assume, that the other beverage is actually not at a discount, otherwise the customer wouldn’t have changed his preferences. It is straightforward, that the lost quantity of the other beverage must be overcompensated with more than equal quantity of mineral water “A”, because of the lower profit margin. Hence, this is another effect, requiring a disproportionate increase of mineral water “A” sold, if we are heading for an economical success out of the discounting.

Hence, if we want to summarize the economical effect of discounting, we cannot simply multiply the (normal- and discount price) quantities with the margins, we also have to account for the different kind of substitution effects.

Additionally we face some fixed costs, that come along with a discounting campaign. They derive from announcements in newspapers, posters and instruction plates in the stores, handling costs, instruction of personnel, reprogramming the scanner cash register etc.

If all those costs (lost margin at the product, different kind of substitution, fixed costs) aren’t really small, or the effect on sold quantity is not extremely high (and not later on compensated in our store), then it is not possible, to achieve an economical benefit out of discounting.

|

About the author: Patrick Mösch is a student in the MSc Program in Business Administration at the University of Bern |

Pricing Blog RSS Feed

Pricing Blog RSS Feed